HF Group has officially crossed the billion-shilling profit line; a turning point signaling its turnaround and entrance into a new phase of scale and competitiveness.

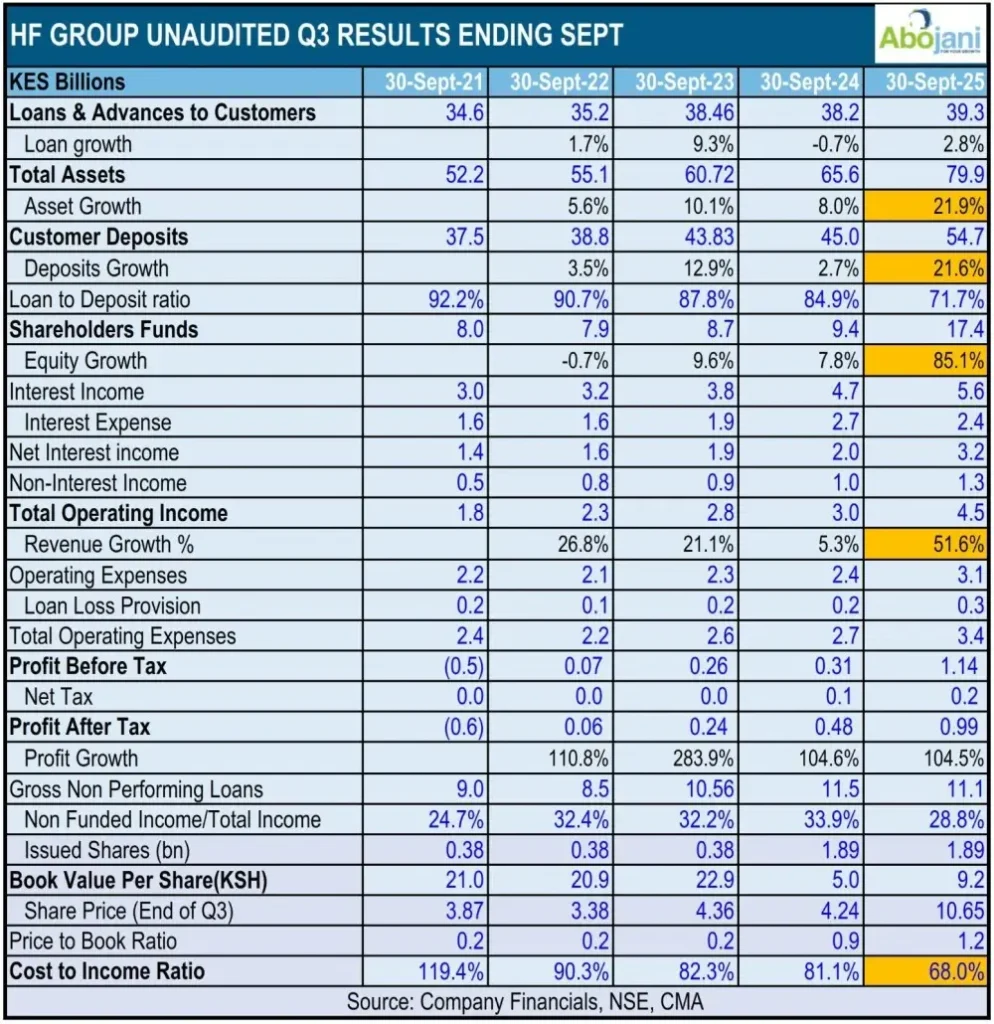

The Group announced a KES 1.14 billion profit before tax for Q3 2025, representing a 265% year-on-year increase up from KES 310 million in Q3 2024. A year-on-year increase of this scale rarely happens in banking without deliberate repositioning, and HF’s results invite a deeper look into the forces pushing the business forward.

Part of the story is efficiency: total operating costs declined by 11% within the same period, falling from KES 900 million to KES 810 million. That cost discipline provides the silent backing that often enables growth to reflect directly in profit.

Total operating income grew by 52%, moving from KES 2.97 billion to KES 4.50 billion. This kind of lift suggests that the business is gaining traction in areas it has spent years building. Total interest income rose by 19%, reaching KES 5.58 billion, owing to interest earned on government securities which nearly doubled; an 85% surge from KES 1.11 billion to KES 2.04 billion. This signals a strategic shift in asset allocation, taking advantage of high-yielding government instruments during a period when retail and corporate lending remains constrained by broader macroeconomic factors.

Non-funded income grew by 29% from KES 1.01 billion to KES 1.30 billion. Growing fee-based and transactional income means the Group is gaining resilience by reducing dependence on interest-rate cycles. This diversification indicates a long-term repositioning that is materializing well.

On the balance sheet side, HF Group added meaningful scale. Total deposits rose by 20%, climbing from KES 45.71 billion to KES 54.74 billion. Assets followed a similar trajectory, growing 22% to KES 79.94 billion. That expansion, paired with the strong liquidity position, gives the Group sufficient room to support lending, invest strategically and withstand market volatility.

The liquidity ratio stood at 26.1% one year ago, barely above regulatory minimums and reflective of a business cautiously managing short-term obligations. As of Q3 2025, that number has more than doubled to 54.2%; a 2.1x jump.

On the capital strength side, core capital to risk-weighted assets ratio moved from 4.3% to 21.9%; more than five times the previous level, and significantly higher than the 10.5% regulatory requirement.

The interplay of these numbers is important. High liquidity paired with strong capital levels indicates a bank that is not over-leveraged. Strong deposit growth paired with rising interest income shows a business able to translate customer traction into revenue. Rising non-funded income alongside declining operating costs signals a maturing business model. When these elements move together, the result is not a lucky quarter; it is a transformation that has begun to compound.

Part of this shift is linked to HF Group’s ongoing diversification strategy. The Group has been open about its long-term goal of reducing dependence on mortgage finance and building an integrated financial ecosystem through HFC, HFDI, HFBI and HF Foundation. The Q3 data suggests that all subsidiaries are beginning to deliver commercial value rather than acting as support functions to the core bank.

The broader market has also taken notice. HF Group’s inclusion in the Morgan Stanley Frontier Markets Small Cap Index (MSCI) earlier this year placed the company on the radar of international investors who track emerging-market performance. The recent elevation of HFC to tier 2 banking status adds to that narrative of institutional strengthening and market relevance.

Beyond the numbers, the Group’s efforts to reduce its base lending rate twice this year reflect a willingness to carry customers along in its recovery. HF Group is signalling a different approach, prioritizing affordability and longer-term relationships over short-term margin protection. Its ongoing digital investments further reinforce a shift toward a more modern, self-service-led customer experience, a critical factor in a market that is increasingly embracing mobile-first financial behaviour.

Taken together, HF Group’s Q3 performance shows it has completed the hardest part of any turnaround: shifting from survival mode to sustainable growth. It is not simply that profits have risen. It is that liquidity has surged, capital buffers have strengthened, deposits have expanded, income has diversified and operational efficiency has improved all at the same time.

HF Group enters the final stretch of 2025 in a markedly stronger position than it has held in years. And if the recent numbers are any indication, the business is no longer climbing out of a difficult period, it is gearing up for scale, stability and strategy.