Imagine running a small profitable business in the CBD, then one random Tuesday morning, you have no business to go to. It could have been a fire, a flood, a break-in, a collapse, forceful closure…This is why business insurance is important for SMEs

This is not unusual for many business owners. It is, in fact, the norm.

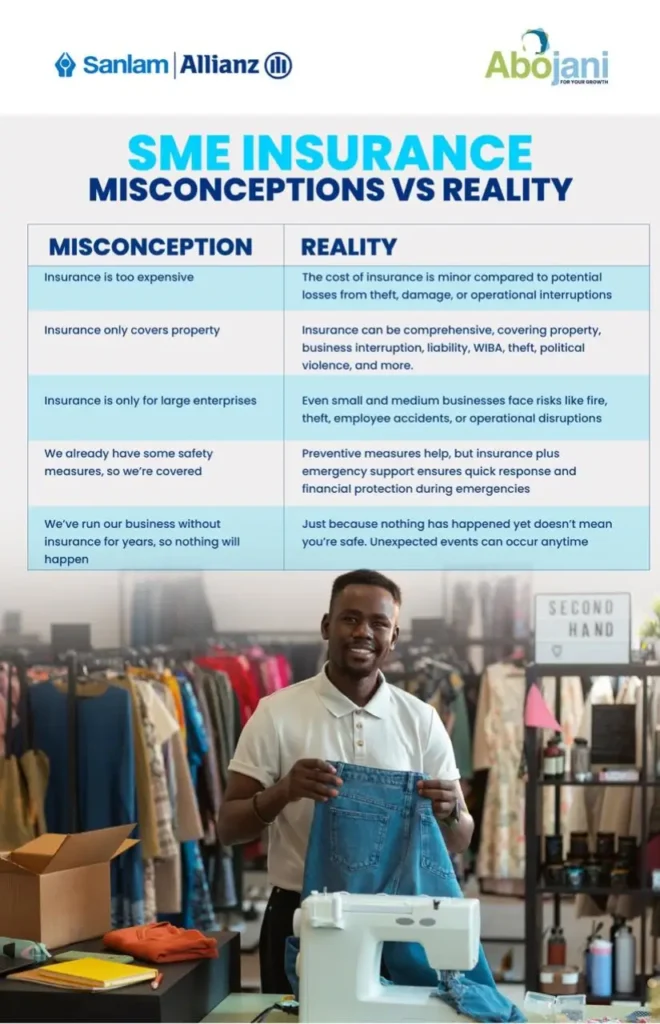

In Kenya, the majority of SMEs operate without comprehensive business insurance. But it isn’t that the owners are reckless, most of them are incredibly hardworking, detail-oriented people. Yet somehow, they file away insurance as a thing to sort out when the business is more stable.

The Real Cost of Operating Without Business Insurance

The costs you see and the ones you don’t

When people think about the cost of being uninsured, they think about the obvious things.

And while replacing machinery, stock, electronics, and furniture out of pocket could wipe out years of retained earnings in a single event, the hidden costs are where most SMEs actually bleed out.

Legal Liability Risks for Small Businesses

Take legal liability. If a customer slips and injures themselves on your premises, or an employee gets hurt on the job, the claim that follows doesn’t care how small your business is. Legal fees, compensation, and settlements can run into millions and without cover, that comes directly from the business.

Many SMEs don’t survive it, not because the incident was catastrophic, but because the financial exposure was.

Then there’s the cost of interruption. A fire doesn’t just destroy your stock; it closes your doors. Every day you’re not operating is revenue you’re not generating, but your rent, loan repayments, and supplier relationships don’t pause with you.

Also Read: How Do You Protect Your Money When Markets Fluctuate?

Business continuity cover exists precisely for this gap, yet most SME owners do not even know it’s an option.

Main Reason why Insurance Matters for Business Growth Opportunities

Here is the opportunity cost. Insurance isn’t just about surviving disasters. Many lenders, corporate clients, and government tenders now require proof of business insurance before they’ll even consider you. Without it, you’re not just unprotected, you’re locked out of growth.

The “it won’t happen to me” math

Risk doesn’t announce itself. The business owner who has operated for five years without incident doesn’t have proof that nothing bad will happen.

Risk doesn’t care about track records. And we’ve seen how quickly situations can escalate, so the question isn’t really if it’s when and how much will it cost.

SME Insurance Solutions in Kenya is Affordable

SME insurance is often far more affordable than business owners expect. A tailored SME package can cover your building, stock, equipment, employees, and liability under one policy and the cost is almost always a fraction of what a single incident would set you back.

A well-structured SME insurance package means that;

➡ When there’s a break-in, you replace the equipment and reopen instead of closing permanently.

➡ When an employee is injured on duty, their medical costs and compensation are handled without gutting your cash flow.

➡ When a corporate client asks for proof of cover before signing, you hand it over without hesitation.

➡ When a riot damages your shopfront, you have a path to recovery.

And when an emergency happens whether it’s an emergency medical situation, a security threat, or a roadside breakdown; tools like SanlamAllianz Emergency Assist (SAZ Assist) mean you will not be scrambling to find help.

You already have it, automatically dispatched to your location. (Learn more about SAZ Assist: https://ke.sanlamallianz.com/general-insurance/emergency-assist)

For every SME owner reading this, ask yourself whether you can afford to be an uninsured business owner, and whether your business could survive it if you were.

You didn’t build this to lose it overnight, so protect it. Start here: https://ke.sanlamallianz.com/general-insurance/individual/sme-insurance

CEO & Co-Founder, Abojani Investment

Robert Ochieng is a visionary entrepreneur and the co-founder of Abojani Investment, a leading financial education platform in Kenya that has empowered over 20,000 Africans to embark on their investment journeys. As CEO, he has demonstrated an unwavering commitment to financial literacy, successfully demystifying money and investments and making them accessible and relevant to individuals from all walks of life.

Running Thriving Investment Communities

Robert’s influence extends well beyond Abojani Investment’s core offerings. He has actively fostered a sense of community by running investment forums and groups with a vast following of over 300,000 Africans. These communities provide a safe space for individuals to exchange ideas, share experiences, and support each other on their investment journeys.

Vision for the Future

As co-founder of Abojani Investment, Robert envisions a financially empowered Africa. He strives to expand the reach of his financial education initiatives, enabling millions more to gain the knowledge and confidence needed to achieve their financial goals. His vision is to create a society where every individual has the tools and understanding to build lasting wealth and prosperity.

Professional Background

Robert Ochieng is a highly accomplished CEO at the helm of Abojani Investment, an investment and advisory firm in Kenya. He is a seasoned professional with over 14 years of experience in IT, Finance, and leadership.

His career includes key roles at prominent institutions such as Equity Bank, Gulf African Bank, Guaranty Trust Bank (GTBank) and Airtel.

Robert’s expertise has also been sought after by the National Treasury for consultancy on planning and budgeting systems, showcasing his exceptional knowledge and skills in the field. Passionate about driving meaningful conversations and collaborations between academia, industry, and the public sector, Robert actively engages in research projects focusing on digital transformation within the financial services sector. With his visionary leadership and strategic insights, Robert Ochieng continues to make a significant impact in the business world.