Absa Bank Kenya delivered a strong set of full-year results for 2025, with profit after tax climbing 10% to KShs 22.9 billion on revenues of KShs 61.4 billion. The board declared a total dividend of KShs 2.05 per share, a 17% increase on the previous year and the bank’s share price closed December at KShs 24.70, up 37% on the previous year, pushing market capitalization to KShs 133 billion.

The headline numbers are solid, but the more interesting story inside these results is structural: Absa Kenya is in the middle of a meaningful business transformation, and 2025 showed it beginning to land.

The profit growth was achieved despite a 6% decline in net interest income (the traditional engine of any commercial bank) as falling Central Bank rates compressed lending margins across the industry. The CBR dropped sharply through the year from 13% in mid-2024 to 8.75% by February 2026, a significant shift that squeezed the interest rate environment for all deposit-taking institutions.

What offset this was disciplined cost-of-funds management; the bank’s cost of funds fell from 5.1% to 3.4% as it optimized its deposit mix, with current accounts now comprising 66% of deposits combined with a 12% surge in non-interest income to KShs 18.1 billion. Non-funded income now represents 29.4% of total revenues, up from 25.8% in 2024.

Operating costs fell 5% to KShs 22.4 billion, continuing a multi-year efficiency drive that has taken the cost-to-income ratio from 46% in 2020 to 36.5% today. Impairment charges dropped 32% to KShs 6.2 billion, reflecting improved portfolio quality, aggressive recoveries, and a tailwind from Kenya’s sovereign rating upgrades, which reduced provisions on government-linked exposures.

The balance sheet grew 6% to KShs 537.6 billion. Customer deposits reached KShs 372.4 billion and customer loans KShs 312.2 billion. Capital and liquidity positions remain well above regulatory thresholds: core capital ratio at 18.3% against a 10.5% minimum, total capital at 21.0%, and liquidity at 45.6% against a 20% floor.

Return on equity came in at 23%, slightly lower than the 24% recorded in 2024 but still running above the bank’s stated target of cost of equity plus 5 percentage points, a benchmark it has consistently met. Shareholders’ funds hit KShs 100.52 billion up from KShs 85.21 billion in 2024.

Absa’s gross NPL ratio fell from 12.3% to 11.4%, at a time when the broader Kenyan banking industry’s NPL ratio sits at 15.5%. The loan loss rate improved from 2.9% to 2.0%, driven by recoveries, improved underwriting, and the positive effect of Kenya’s sovereign rating upgrade on government-linked exposures.

Total customer loans grew just 1% to KShs 312.2 billion. Corporate Banking loans grew 5%, but Consumer and Business Banking loans contracted 2%, reflecting sustained pressure on household disposable incomes in Kenya’s tough consumer environment.

The Wealth and Asset Management Story

Perhaps the most striking data point in the entire results pack is the trajectory of Absa’s asset management business.

Two years ago, the bank’s money market fund ranked 26th in Kenya. It now ranks 3rd, with assets under management growing 53% YoY to KShs 46 billion. Assets under custody surged from KShs 4 billion in 2024 (launch) to over KShs 70 billion; an 18-fold increase in a single year.

This reflects a strategic repositioning. In 2025 the bank launched Absa Wealth, a full wealth management proposition aimed at the upper end of the consumer market, alongside enhancements to its Prestige and Premier banking offerings. The Bancassurance business maintained its number one ranking by profitability. Brokerage revenues grew 44% and asset management revenues grew 97%.

These new businesses contributed 7% of total income in 2025, up from 6% the year before. In absolute terms that is KShs 4.3 billion, growing 17% year-on-year.

The significance of this shift is twofold. First, wealth and fee-based income is less sensitive to interest rate cycles than net interest income, making the overall earnings base more resilient. Second, the Kenyan wealth management market remains underpenetrated relative to the size of the country’s high-net-worth and upper-middle-income segments. Absa is positioning early and at scale.

A Corporate Bank Winning Big Mandates

The Corporate and Investment Banking division delivered some of the most visible results of the year. Absa Kenya acted as financial adviser and led multiple multi-billion transactions, like the $3 billion acquisition of Diageo’s controlling stake in East Africa Breweries Limited by Asahi Group Holdings.

The FX business delivered a standout performance, with market share in foreign exchange revenues jumping from 9% (ranking 6th in the industry) to 15% (ranking 2nd) in the space of a year. The bank attributes this to strong client adoption of its digital Personalized FX platform, alongside expansion of its Emerge product suite for risk management and yield enhancement.

The CIB division’s share of total group profitability rose to 26% in 2025, up from prior years, reflecting the growing contribution of these high-margin, fee-based business lines.

The Digital and Efficiency Engine

The bank reports that 71% of customer processes are now digitized, up from 65% in 2024, and 94% of all transactions are conducted through alternative channels. Back-office automation delivered over 80,000 man-hours of savings in 2025, double the 2024 figure.

Digital lending through Timiza, the bank’s mobile credit platform, grew revenues 19% to KShs 1.8 billion. The ecosystem banking platform for SMEs doubled its client base and delivered 18x growth in lending drawdowns. Over 40,000 SMEs were reached through capacity-building initiatives.

These investments are self-funding through the efficiency gains they generate. Technology spend actually fell slightly from KShs 1.28 billion to KShs 1.16 billion year-on-year, even as the digitisation level improved, suggesting the bank is extracting better returns per shilling of technology investment. The sustained cost-to-income improvement from 38% in 2024 to 36.5% in 2025 reflects this dynamic.

In Business Banking, the bank marked 20 years of Islamic banking operations and expanded its Shariah-compliant La Riba product suite, including a new La Riba credit card. Merchant payments through Lipa na Absa grew 250%.

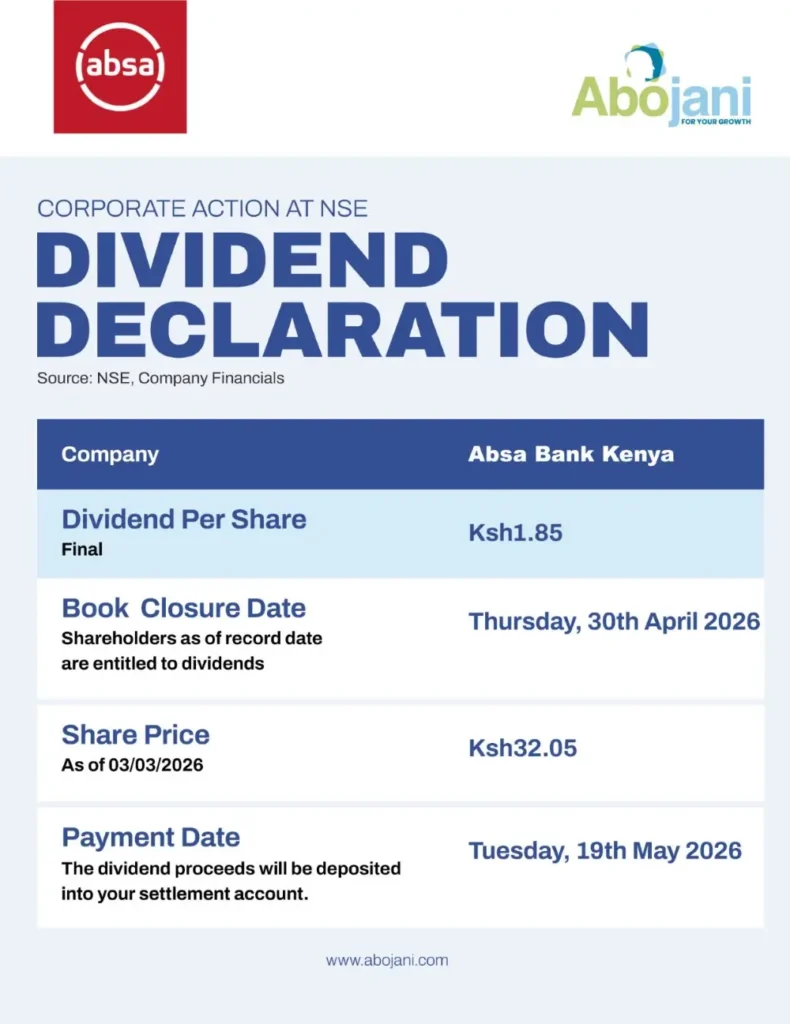

The final dividend of KShs 1.85 per share will be paid on or around 19 May 2026 to shareholders on record as of 30 April 2026, with the total 2025 dividend of KShs 2.05 per share representing the fifth consecutive year of dividend growth.

Absa Bank Kenya’s FY2025 results tell the story of a bank managing a transitional moment in its income mix with considerable skill.