SACCOs have long been a trusted way for many people to save, access credit, and grow wealth collectively. However, knowing how to choose a SACCO in Kenya requires looking past the surface. The dividend is often one of the most visible measures of success, and it’s tempting to choose a SACCO promising high payouts. But as John Mwangi, CEO of Tai SACCO Society Ltd, explained at Abojani’s 4th Economic Empowerment Conference, high dividends can be misleading.

A SACCO that pays out more than it earns may look attractive in the short term, but over time, this can weaken its financial foundation and leave members exposed when they need loans or support the most.

Also read: Focus on thriving SACCO landscape

This is why due diligence is crucial. Before joining, it’s important to understand how the SACCO operates, starting with the basics.

1. What is the minimum share capital required to become a member?

2. What does this financial commitment mean for your budget and long-term financial planning?

3. How consistent have past dividends been, and are they driven by sustainable profits or one-time decisions?

Knowing the interest rates on deposits and the lending capacity of the SACCO helps you evaluate how your money will work for you and what access to credit looks like when you need it.

Loan terms are equally important. Understanding what collateral or guarantees are required ensures you are not exposed to unexpected obligations. Membership fees should also be reasonable, reflecting the value you receive without unnecessarily reducing your returns. Beyond the numbers, it’s essential to consider reputation, governance, and service quality.

How transparent is the SACCO? Are policies, by-laws, and regulations clearly communicated and consistently applied? A strong, experienced management team often signals stability and accountability, and that matters for long-term wealth building.

Core Financial Metrics to Check Before you choose a SACCO

High dividends can sometimes be funded out of current cash reserves rather than actual retained earnings, which weakens the institution over the long term. To ensure you are choosing a stable partner, you must look closely at their audited financial statements for these two foundational indicators:

Share Capital vs. Member Deposits

It is critical to understand the operational difference between these two pools of money:

- Share Capital: This is non-withdrawable. It represents your permanent equity ownership in the SACCO. You cannot use it to guarantee loans, and it can only be sold or transferred to another member if you decide to leave the institution.

- Member Deposits: These are withdrawable (usually subject to a 60-day written notice). This is the pool of savings used to collateralize your loans and calculate your borrowing multiplier. A financially healthy, well-balanced SACCO grows both of these metrics proportionately year over year.

Institutional Capital

Think of institutional capital as the SACCO’s built-in financial cushion. It consists of retained earnings and statutory reserves that the institution holds to weather economic downturns. If a SACCO’s institutional capital is low but its dividend payouts are exceptionally high, it is a massive red flag. The institution is essentially eating into its own future stability just to keep members happy short-term.

Lending Capacity and Liquidity: Can You Actually Get a Loan?

Most Kenyans join a SACCO specifically for the “multiplier effect”—the ability to borrow three to four times their savings. However, one of the most common frustrations for savers is waiting months for a loan to be disbursed because the SACCO is facing a liquidity crunch.

Before you hand over your money, do two things:

- Ask about their actual Loan Turnaround Time for development and emergency loans.

- Review their Net Loans-to-Deposits ratio. If a SACCO has lent out 95% or more of its total member deposits, it has very little liquid cash on hand. This means it may struggle to clear your loan quickly when you need emergency funding.

Watch this discusion for the different tools and skiils you need before you choose a sacco :

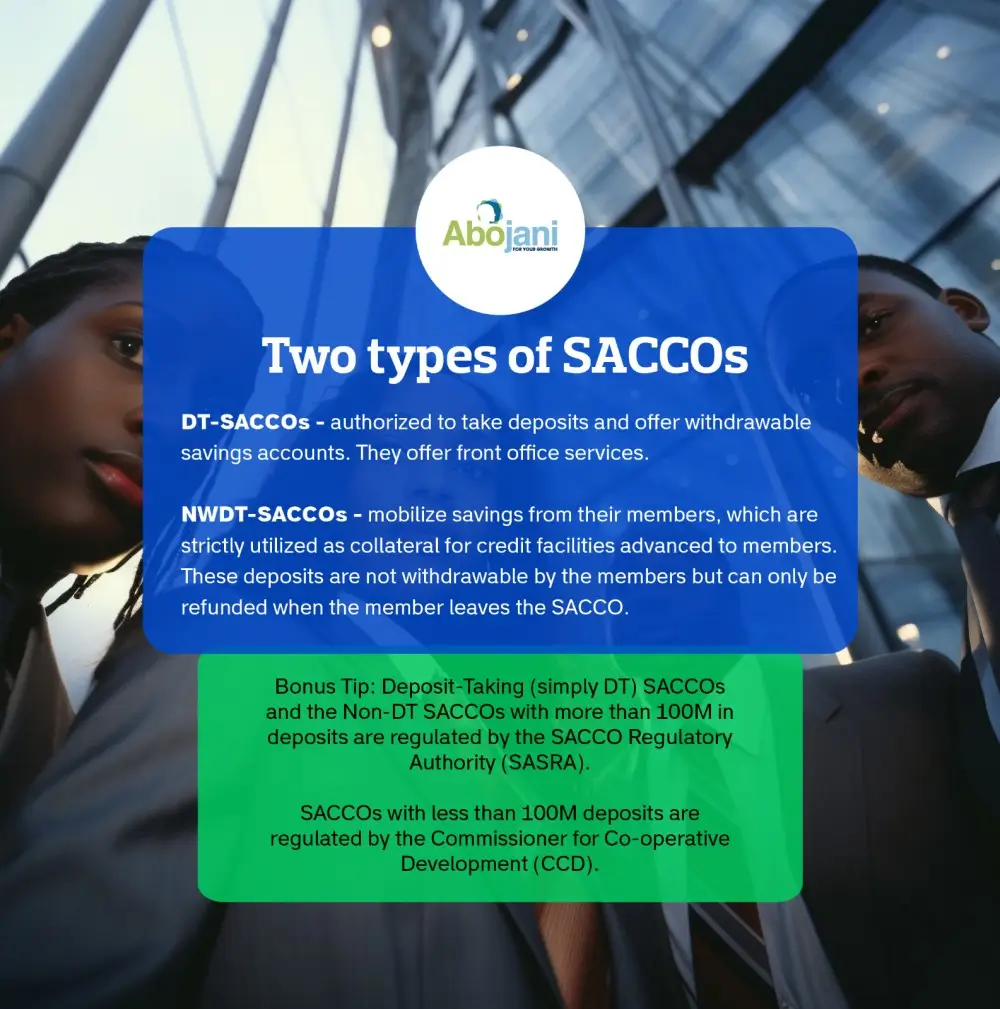

Governance and Regulatory Compliance (SASRA)

Financial stability is entirely dependent on governance. In Kenya, poor governance often manifests as high default rates and unmanaged insider lending—where board members or staff receive large loans without proper collateral.

Critical Verification Step: Any serious, deposit-taking SACCO in Kenya must be licensed and regulated by the Sacco Societies Regulatory Authority (SASRA).

SASRA enforces strict compliance guidelines regarding capital adequacy, liquidity buffers, and management behavior. Before joining any institution, always check the updated official SASRA registry online to confirm that the SACCO’s license is active, unrestricted, and in good standing.

Tech and Accessibility: Digital Banking Infrastructure

A competitive dividend rate matters very little if you still have to physically travel to a brick-and-mortar branch or fill out manual paper forms every time you want to guarantee a friend’s loan, check your balance, or top up your deposits.

Modern financial planning requires speed and accessibility. When evaluating a SACCO, closely examine their digital ecosystem:

- Is their mobile banking app functional, reliable, and secure?

- Do they have a robust, active USSD shortcut for quick transactions?

- How seamless is their integration with M-Pesa for real-time deposits and withdrawals?

In today’s economy, convenience isn’t a luxury—it’s a basic requirement for effective wealth management.At its core, When you choose a SACCO is not just about chasing the highest short-term dividend. A well-managed SACCO can provide access to loans, encourage disciplined saving, and create opportunities for wealth accumulation in ways that are reliable and safe. Members who take the time to evaluate financial health, governance, and services position themselves to benefit for years to come.

High dividends may catch the eye, but the real measure of a SACCO’s strength is in its transparency, financial stability, and member-centered practices. Asking the right questions and understanding how a SACCO operates is an important step in protecting your money and building lasting financial security.

#Joining a SACCO #Economic Empowerment COnference

CEO & Co-Founder, Abojani Investment

Robert Ochieng is a visionary entrepreneur and the co-founder of Abojani Investment, a leading financial education platform in Kenya that has empowered over 20,000 Africans to embark on their investment journeys. As CEO, he has demonstrated an unwavering commitment to financial literacy, successfully demystifying money and investments and making them accessible and relevant to individuals from all walks of life.

Running Thriving Investment Communities

Robert’s influence extends well beyond Abojani Investment’s core offerings. He has actively fostered a sense of community by running investment forums and groups with a vast following of over 300,000 Africans. These communities provide a safe space for individuals to exchange ideas, share experiences, and support each other on their investment journeys.

Vision for the Future

As co-founder of Abojani Investment, Robert envisions a financially empowered Africa. He strives to expand the reach of his financial education initiatives, enabling millions more to gain the knowledge and confidence needed to achieve their financial goals. His vision is to create a society where every individual has the tools and understanding to build lasting wealth and prosperity.

Professional Background

Robert Ochieng is a highly accomplished CEO at the helm of Abojani Investment, an investment and advisory firm in Kenya. He is a seasoned professional with over 14 years of experience in IT, Finance, and leadership.

His career includes key roles at prominent institutions such as Equity Bank, Gulf African Bank, Guaranty Trust Bank (GTBank) and Airtel.

Robert’s expertise has also been sought after by the National Treasury for consultancy on planning and budgeting systems, showcasing his exceptional knowledge and skills in the field. Passionate about driving meaningful conversations and collaborations between academia, industry, and the public sector, Robert actively engages in research projects focusing on digital transformation within the financial services sector. With his visionary leadership and strategic insights, Robert Ochieng continues to make a significant impact in the business world.