Walk into any Kenyan town today and you’ll notice two kinds of bank customers.

There’s the Gen Z professional who hasn’t stepped into a banking hall in years … everything from paying suppliers, sending rent, and even applying for quick credit happens on their smartphone. For them, banking is a digital-first experience, fast, seamless, and always available.

Then there’s the SME owner, the farmer, or the family business patriarch who still values walking into a branch, sitting across from their Relationship Manager, and having an in-depth conversation about a business loan, cashflow challenges, or investment opportunities. For them, banking is about trust, human connection, and being heard.

Traditionally, these two worlds were kept apart. Digital banking for convenience, branch banking for relationships. But in recent years, the banking landscape has really evolved. We are now seeing phygital strategies, that is, the seamless combination of physical and digital banking.

The shift to phygital banking is mostly about customer expectations. Time-starved customers want 24/7 access to services without queues or paperwork. Relationship-driven customers still need the reassurance of in-person consultation. SMEs and corporates require both: the speed of digital transactions, but also expert human guidance on financing decisions.

Phygital banking acknowledges that customers don’t fit into one box. They move between digital and physical depending on context, and banks must move with them.

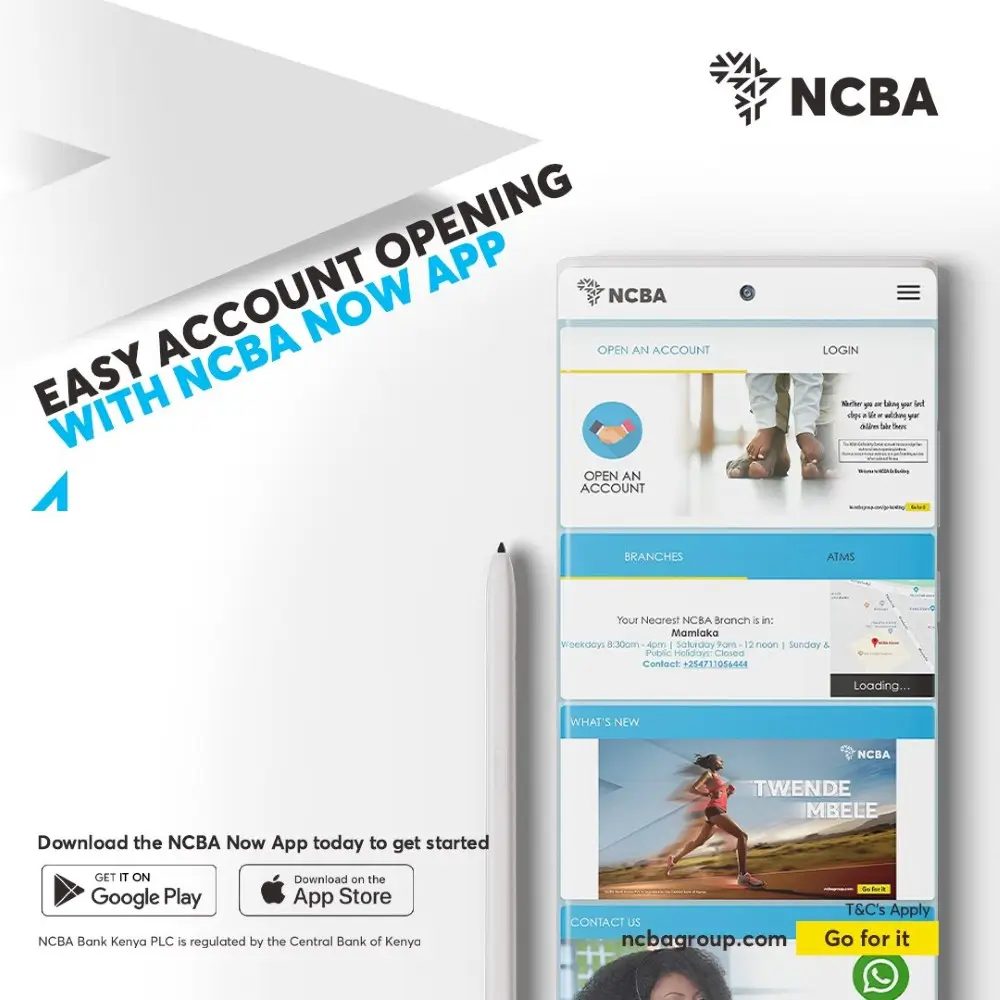

NCBA Bank has been one of the biggest banks in Kenya to embrace this dual strategy, weaving digital convenience into the fabric of its traditional strengths. Through the NCBA Now App, customers enjoy real-time account management, instant transfers, loan applications, and investment options, all from their smartphones.

At the same time, branches remain strong pillars of trust, especially in regions like Kerugoya, Karatina, and Nyeri, where customers engage directly with Relationship Managers on asset financing, mortgages, and SME solutions.

This dual offering ensures that a customer who checks balances digitally today can comfortably walk into a branch tomorrow for a complex consultation without friction.

During NCBA’s recent Central Region Engagement Tour, senior leadership including James Gossip (MD, NCBA Kenya) and Dennis Njau (Group Director, Retail Banking) met customers face-to-face, reaffirming the value of physical presence even in a digital era.

NCBA’s phygital approach is about human-centered banking. For the boda rider or trader in Karatina who needs quick working capital, digital channels provide speed. For the Nyeri-based SME expanding into manufacturing, branch-based Relationship Managers provide depth and trust. For families investing in unit trusts or mortgages, NCBA offers both, guidance in person and convenience online.

By merging physical and digital, NCBA is also driving financial inclusion. In underserved areas, branches anchor trust, while digital platforms extend reach. A customer in rural Kirinyaga can access NCBA’s solutions without always needing to travel, but still knows that an expert is within reach. This hybrid model ensures that no one is left behind, neither the tech-savvy Gen Z investor nor the traditional SME client who values eye contact and conversation.

That is the very promise of phygital banking. In the end, the future of banking isn’t physical or digital. It’s both.