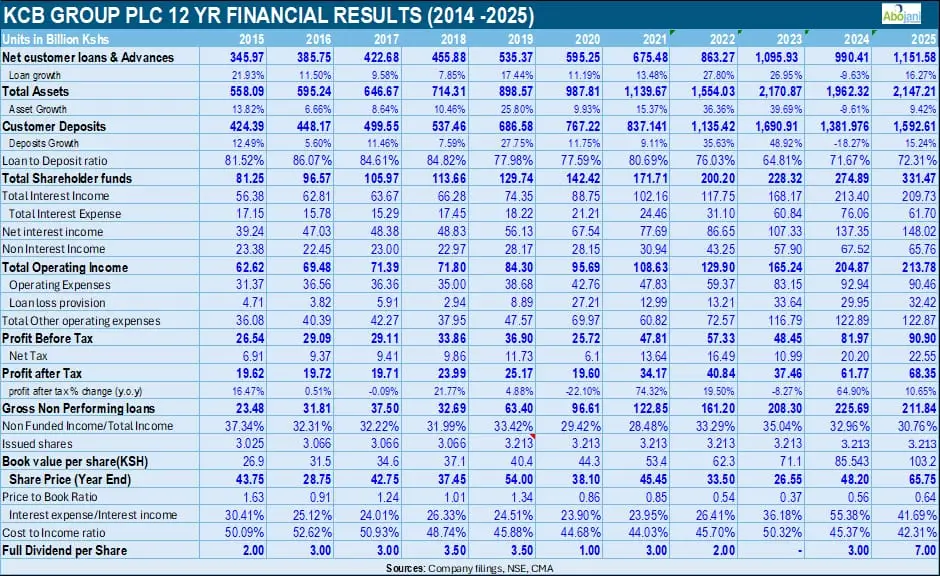

KCB Group Plc ended 2025 on a high, posting a record profit after tax (PAT) of KShs. 68.4 billion for the full year, an 11% jump from the KShs. 61.8 billion recorded in 2024. The results confirm the Group’s trajectory as it deepens its regional footprint and accelerates its transformation into a digitally led financial services provider across East Africa.

The final quarter of 2025 pushed the 2025 topline numbers to all time highs for the lender. Full-year profit before tax (PBT) came in at KShs. 90.9 billion, up 11% year-on-year, with the balance sheet growing 9.3% to KShs. 2.15 trillion; a milestone achieved even after completing the sale of National Bank of Kenya to Access Bank in May 2025.

The divestiture, which would ordinarily have weighed on asset growth, was more than offset by new-to-bank business across corporate and retail segments, underscoring the resilience of the Group’s diversified model.

The Regional Engine

One of the defining themes of the 2025 result is how broadly the growth was shared across the Group’s seven-country footprint. Subsidiaries outside KCB Bank Kenya contributed 30.5% of the Group’s balance sheet and 30.7% of profit before tax, with total assets in those subsidiaries rising 20% during the year.

Trust Merchant Bank (TMB) in the DRC contributed KShs. 8.5 billion in after-tax profit, though this was 18% lower year-on-year partly due to the temporary closure of some branches in Eastern DRC, which also clipped the Group’s foreign exchange income. BPR Bank Rwanda grew profit 23%, KCB Bank Tanzania surged 25%, and KCB Bank Uganda was up 58%. The non-banking subsidiaries also put in a strong showing: KCB Bancassurance Intermediary grew PBT 29 % to KShs. 1.14 billion, KCB Investment Bank rose 31%, and KCB Asset Management climbed 54%.

The Group serves 34 million customers; 11 million through conventional banking and 23 million digitally, across 456 branches and 1,249 ATMs, with 1.3 million agents and merchants completing the last-mile distribution network.

Digital Transformation

KCB’s investment in digital channels is increasingly showing up in the revenue line. Mobile loan disbursements grew 30% to KShs. 544 billion during the year, equivalent to KShs. 1.1 billion disbursed every single day. Lending fees rose 18 % on the back of this surge in digital credit. An overwhelming 99% of all transactions by number were processed through non-branch channels, reflecting how thoroughly customers have migrated to digital and agency platforms.

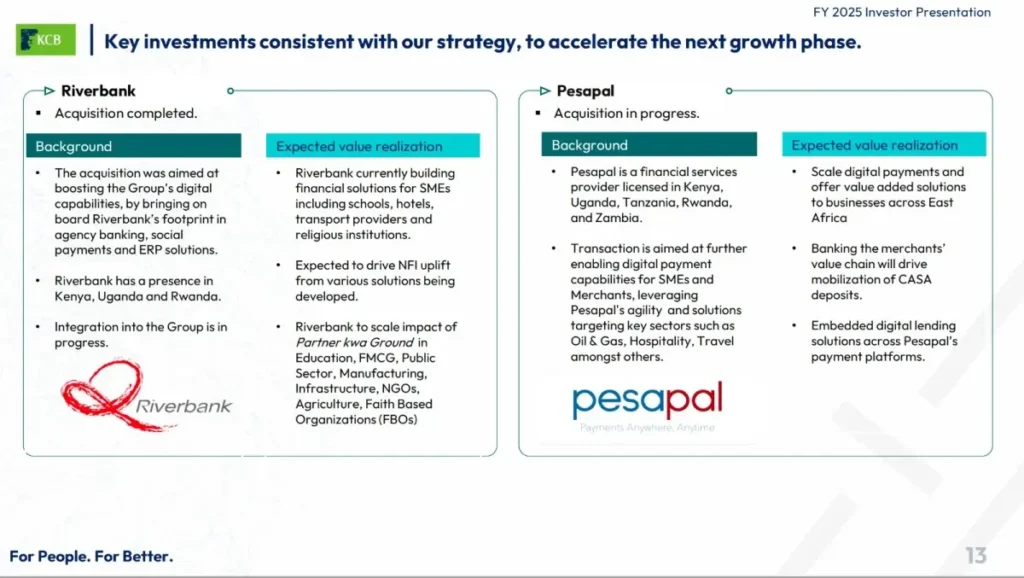

The Group also launched a new unified mobile app during the year, featuring self-onboarding for accounts and wallets, integrated money market fund access, and a mini-app ecosystem. On the payments side, KCB introduced a multicurrency prepaid card supporting 18 currencies and signed up to PAPSS, enabling seamless cross-border payments across the continent.

The ongoing acquisition of a minority stake in Pesapal Ltd; a payments technology firm licensed across Kenya, Uganda, Tanzania, Rwanda, and Zambia, is expected to further deepen KCB’s digital payments infrastructure once regulatory approvals are concluded.

Cost Discipline

The cost-to-income ratio fell to 42.3% from 45.4% in 2024, the best efficiency reading the Group has recorded in years. Total operating expenses declined 3% year-on-year to KShs. 90.5 billion, even as revenues grew 4% to KShs. 213.8 billion, generating a positive jaws ratio of 7 percentage points.

The improvement was driven by the exit from NBK which carried its own cost base, as well as deliberate efforts to leverage shared Group capabilities, deploy robotic process automation across business lines, and optimize the branch network. Staff costs fell 2.2 %, depreciation and amortisation declined 10.6%, and the staff cost-to-income ratio improved to 18.2% from 19.5%.

Net interest income, which forms the backbone of revenues, grew 8% to KShs. 148 billion as the Group benefited from a meaningful 19% decline in its interest expense, reflecting lower funding costs as central bank rates in its key markets began to ease.

Loan Quality

KCB’s asset quality metrics showed meaningful improvement in 2025 with the Group NPL ratio declining to 16.9% from 19.2% at end-2024, and the gross NPL stock falling KShs. 14 billion during the year to close at KShs. 211.8 billion.

Coverage also strengthened considerably. The regulatory NPL coverage ratio rose to 122.4% from 101.2% in 2024, meaning the entire non-performing book is more than fully covered by provisions and collateral held. IFRS coverage improved to 113.2% from 92.3%. Sectorally, the personal and household book, which is the largest single segment at 29.6% of gross loans, saw its NPL ratio drop to 8.4%.

At a subsidiary level, KCB Bank Uganda recorded the sharpest improvement, with its NPL ratio more than halving to 5.9% from 6.8% in 2024; KCB Bank Tanzania and KCB Bank Burundi also improved. KCB Bank Kenya remains the biggest pocket of stress at a 19.9% NPL ratio, though this too is trending in the right direction.

Record Dividend

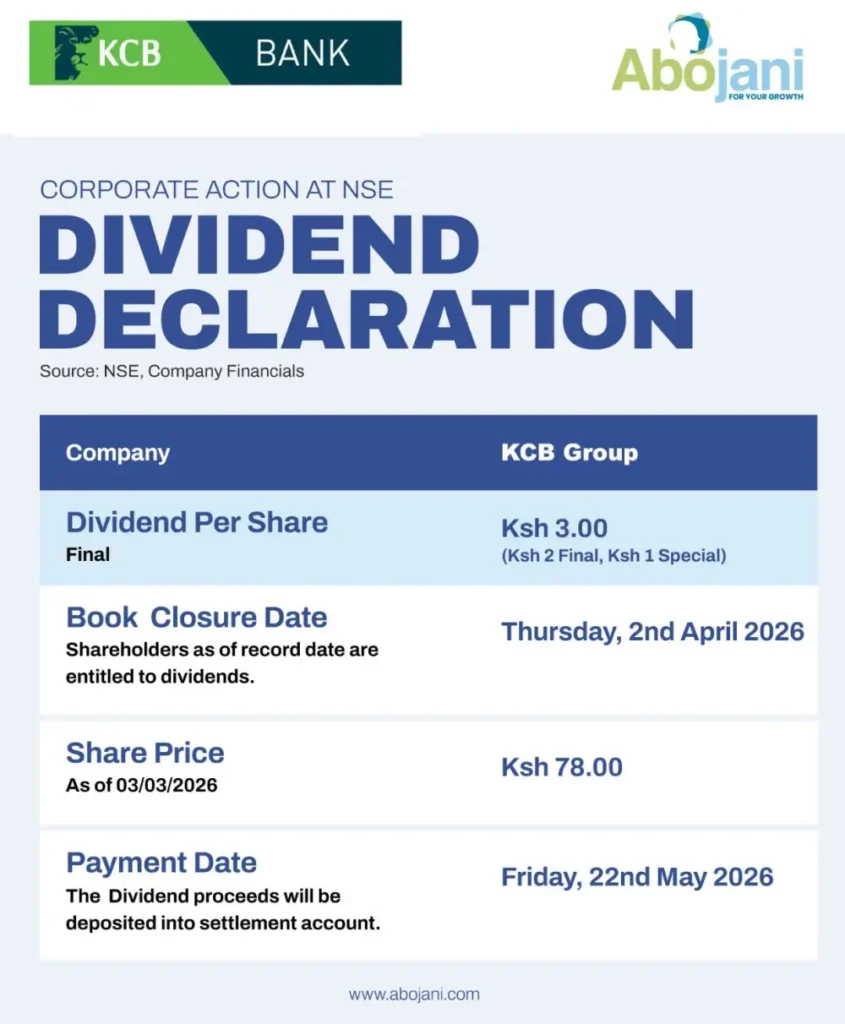

For shareholders, 2025 marks a landmark year. The Board has recommended a final dividend of KShs. 3.00 per share, subject to approval at the Annual General Meeting. Combined with the KShs. 4.00 interim dividend; which comprised KShs. 2.00 interim and a KShs. 2.00 special dividend paid in November 2025, the total payout for the year comes to KShs. 7.00 per share, or KShs. 22 billion in aggregate.

That is a 133 % jump from the KShs. 3.00 total dividend paid in respect of 2024, and the largest absolute dividend in the Group’s history.

The dividend news arrives against a backdrop of strong share price performance. KCB’s stock closed 2025 at KShs. 65.75, up 58% from KShs. 41.60 at end-2024, lifting the Group’s market capitalization to KShs. 211 billion. Including dividends, total shareholder return for the year stood at 75%. Earnings per share rose 12% to KShs. 20.79, while shareholders’ equity grew 21% to KShs. 331.5 billion. Return on equity held at 22.5%.

“Our 2025 performance reflects the strength of the KCB franchise, the resilience of our regional footprint, and the continued trust that customers place in us.” Paul Russo, Group CEO, KCB Group Plc

Looking into 2026, with its balance sheet now comfortably above KShs. 2 trillion, its NPL trajectory improving, its cost engine well-tuned, and a record dividend on the table, KCB is moving from a position of considerable strength.

#KCB2025FYResults #ForPeopleForBetter #Profit After Tax #Follow Abojani

CEO & Co-Founder, Abojani Investment

Robert Ochieng is a visionary entrepreneur and the co-founder of Abojani Investment, a leading financial education platform in Kenya that has empowered over 20,000 Africans to embark on their investment journeys. As CEO, he has demonstrated an unwavering commitment to financial literacy, successfully demystifying money and investments and making them accessible and relevant to individuals from all walks of life.

Running Thriving Investment Communities

Robert’s influence extends well beyond Abojani Investment’s core offerings. He has actively fostered a sense of community by running investment forums and groups with a vast following of over 300,000 Africans. These communities provide a safe space for individuals to exchange ideas, share experiences, and support each other on their investment journeys.

Vision for the Future

As co-founder of Abojani Investment, Robert envisions a financially empowered Africa. He strives to expand the reach of his financial education initiatives, enabling millions more to gain the knowledge and confidence needed to achieve their financial goals. His vision is to create a society where every individual has the tools and understanding to build lasting wealth and prosperity.

Professional Background

Robert Ochieng is a highly accomplished CEO at the helm of Abojani Investment, an investment and advisory firm in Kenya. He is a seasoned professional with over 14 years of experience in IT, Finance, and leadership.

His career includes key roles at prominent institutions such as Equity Bank, Gulf African Bank, Guaranty Trust Bank (GTBank) and Airtel.

Robert’s expertise has also been sought after by the National Treasury for consultancy on planning and budgeting systems, showcasing his exceptional knowledge and skills in the field. Passionate about driving meaningful conversations and collaborations between academia, industry, and the public sector, Robert actively engages in research projects focusing on digital transformation within the financial services sector. With his visionary leadership and strategic insights, Robert Ochieng continues to make a significant impact in the business world.