Pension savings in Kenya have quietly grown into one of the most powerful but underused engines of wealth creation. When John Keah, Deputy Director of Market Conduct & Industry Development at the Retirement Benefits Authority (RBA), took the stage at the 5th Abojani Economic Empowerment Conference, he challenged us with a question.

“What else can retirement benefits do beyond just the saving aspect to bring about economic prosperity?”

Today, Kenya has more than 30 million working citizens, yet only 7.53 million are actively saving for retirement. Pension coverage stands at just 26.5% of the working-age population. This means that nearly three out of every four working Kenyans are moving through their earning years without deliberately preparing for a future where employment income may no longer exist.

The implications extend beyond individuals.

Also read: The Importance of Early Retirement Planning: Understanding Pension Fund Options

“If we do nothing about it,” Keah noted, “the reality is that we are the ones who will cater to those who have not prepared.”

Why Pension Savings Matter for Every Working Kenyan

Retirement should not be viewed as an age. It can happen because someone decides they have worked long enough and want to pursue other interests. It can arrive through ill health. Sometimes it comes because circumstances simply change.

The reality is that retirement is often unpredictable.

Keah emphasized that the objective of saving through a retirement scheme is not merely to survive once employment ends. It is to ensure that individuals can continue to thrive regardless of when retirement arrives.

The Wealth Creation Power of Retirement Planning

Retirement planning carries a powerful wealth proposition.

Income Replacement and Long-Term Security

At the most obvious level, it is an important vehicle for wealth creation and income replacement. International standards advocate for retirement income that replaces at least 40% of a person’s pre-retirement earnings. In Kenya, the replacement ratio is closer to 30%.

Yet the benefits extend beyond finances.

Psychological and Health Benefits

Retirement planning also offers psychological benefits. Building financial security for the future helps reduce uncertainty and anxiety about later life.

There is also a physiological dimension. Good health and financial wellbeing are deeply interconnected. Recognizing this, the authority has introduced initiatives such as the post-retirement health fund to support retirees beyond their working years.

Social Independence

The social dimension is equally important. Retirement planning helps individuals maintain independence and manage expectations around financial support from family members. In doing so, it can reduce the pressures that often accompany intergenerational financial obligations.

How Pension Savings Fuel Kenya’s Economy

Retirement schemes can help mobilize long-term capital that can be invested productively throughout the economy.

15 Asset Classes Available to Retirement Schemes

Retirement schemes in Kenya can invest across fifteen different asset classes. Most pension assets are concentrated in four primary asset classes: equities, government securities, property, and deposits. However, emerging opportunities such as infrastructure investments and REITs continue to broaden the investment landscape.

Patient Capital for National Development

This means pension savings serve two purposes simultaneously. For individuals, they help build wealth and provide financial security. For the country, they create pools of patient capital that can finance major investments, stimulate economic activity, and contribute to long-term development.

How Retirement Schemes Work

Pension contributions do not disappear into a single institution. Retirement schemes operate through a system of specialized professionals, each with distinct responsibilities.

Trustees, Custodians, Fund Managers, and Administrators

Trustees carry the fiduciary responsibility of acting in the best interests of members and overseeing the scheme.

Custodians, typically banks, receive and safeguard contributions.

Fund managers then make investment decisions, determining how those funds should be allocated across various asset classes.

Administrators manage records, documentation, and member accounts.

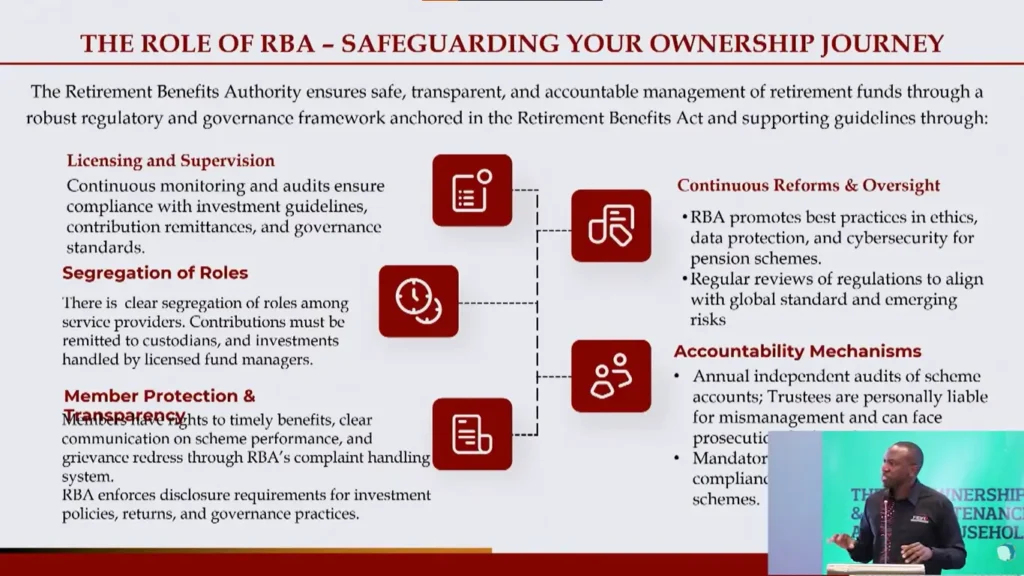

This segregation of responsibilities creates multiple layers of accountability and protection.

The industry is also supported by continuous reporting requirements, consumer education initiatives, complaints resolution mechanisms, regulatory reforms, and ongoing oversight by the Authority.

The objective is simple: to ensure retirement savings are properly governed, protected, and managed responsibly.

The Role of the Retirement Benefits Authority

KSh 2.5 Trillion Under RBA Oversight

The Retirement Benefits Authority was established through an Act of Parliament and began operations in 2000. Today, it oversees more than 1,000 registered retirement schemes across the country.

As of June 2025, retirement schemes had accumulated KSh2.5 trillion in savings, equivalent to approximately 15 percent of Kenya’s Gross Domestic Product. These funds represent the cumulative savings of 7.53 million Kenyans.

The Authority’s role goes beyond regulation. It undertakes substantial research to ensure policies remain sound, relevant, and beneficial to citizens. It also seeks to expand pension coverage, particularly among workers in the informal sector who have traditionally had limited access to retirement products.

As Keah explained, pensions present an opportunity to grow wealth, and increasing access to retirement savings remains one of the Authority’s key priorities.

Expanding Coverage to the Informal Sector

Historically, retirement schemes have primarily served workers in the formal sector through occupational pension arrangements. However, the labour market is changing, and traditional employment structures no longer reflect the realities of how many people earn their income.

Recognizing this shift, the Retirement Benefits Authority is pursuing policies and strategies that support more inclusive and flexible retirement solutions. This includes individual pension schemes and flexible post-retirement products such as income drawdown arrangements.

The Authority is also placing increased emphasis on consumer protection while expanding its focus on solutions that address the evolving needs of different market segments.

A Call to Action: Become a Retirement Planning Ambassador

The keynote closed with a call to action.

Retirement planning cannot remain a conversation reserved for a minority of workers or for people approaching the end of their careers.

The future may arrive by choice, by circumstance, or by necessity. We must therefore become ambassadors for this message, encouraging not only our own retirement preparedness but also helping those around us.

CEO & Co-Founder, Abojani Investment

Robert Ochieng is a visionary entrepreneur and the co-founder of Abojani Investment, a leading financial education platform in Kenya that has empowered over 20,000 Africans to embark on their investment journeys. As CEO, he has demonstrated an unwavering commitment to financial literacy, successfully demystifying money and investments and making them accessible and relevant to individuals from all walks of life.

Running Thriving Investment Communities

Robert’s influence extends well beyond Abojani Investment’s core offerings. He has actively fostered a sense of community by running investment forums and groups with a vast following of over 300,000 Africans. These communities provide a safe space for individuals to exchange ideas, share experiences, and support each other on their investment journeys.

Vision for the Future

As co-founder of Abojani Investment, Robert envisions a financially empowered Africa. He strives to expand the reach of his financial education initiatives, enabling millions more to gain the knowledge and confidence needed to achieve their financial goals. His vision is to create a society where every individual has the tools and understanding to build lasting wealth and prosperity.

Professional Background

Robert Ochieng is a highly accomplished CEO at the helm of Abojani Investment, an investment and advisory firm in Kenya. He is a seasoned professional with over 14 years of experience in IT, Finance, and leadership.

His career includes key roles at prominent institutions such as Equity Bank, Gulf African Bank, Guaranty Trust Bank (GTBank) and Airtel.

Robert’s expertise has also been sought after by the National Treasury for consultancy on planning and budgeting systems, showcasing his exceptional knowledge and skills in the field. Passionate about driving meaningful conversations and collaborations between academia, industry, and the public sector, Robert actively engages in research projects focusing on digital transformation within the financial services sector. With his visionary leadership and strategic insights, Robert Ochieng continues to make a significant impact in the business world.