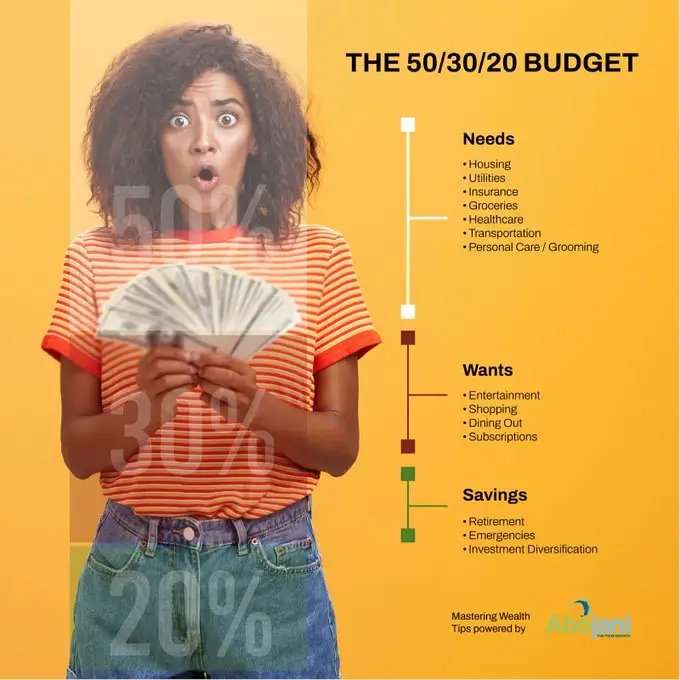

The 50/30/20 budgeting rule was popularized by US senator Elizabeth Warren and her daughter Amelia Warren Tyagi, in the book “All Your Worth”. It is meant to help you organize your financials around your needs, wants and investments.

The 50/30/20 Budgeting Rule Explained

50% of you income should go to needs such as rent, utility bills, grocery, shopping, transports, car fuel etc

30% of your net income should go to your wants or self-development needs. This is the layer that builds the body, mind and soul and includes spending on leisure, entertainment, tithe, financial support for friends and family, self-education, networking, industry association membership subscriptions etc. The spending in this part should help you become a better person and grow your social capital over time.

Also Read: Budgeting as a Self-Awareness Tool

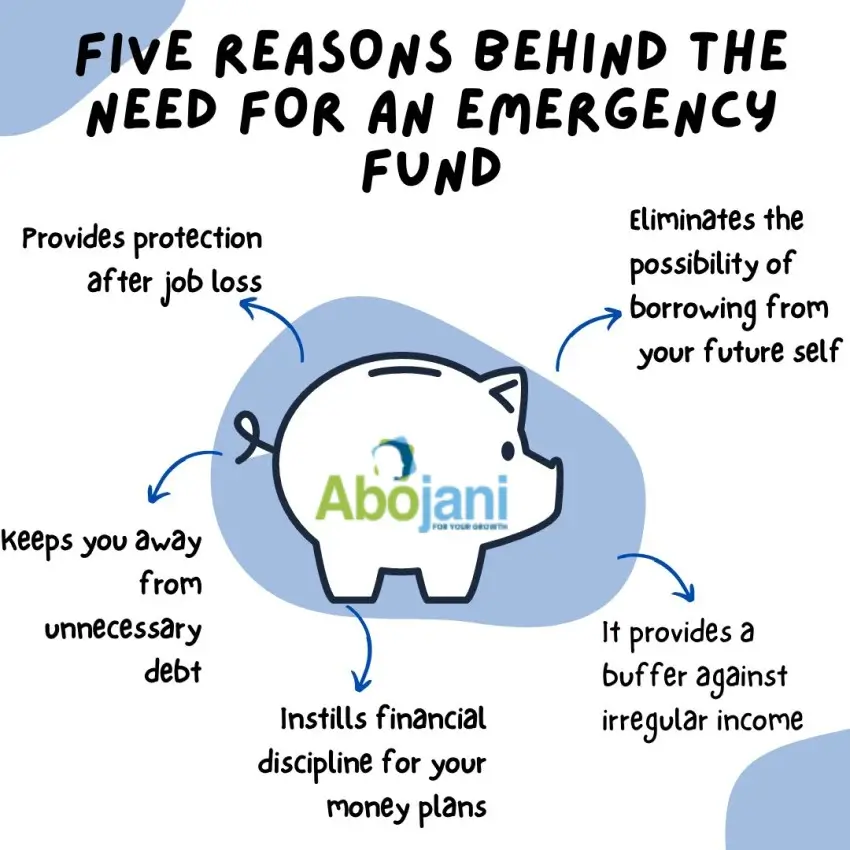

20% of your net income should go to savings and investments. Savings and investments will help you with your short-term and long-term goals such as starting a business, buying a car, building a house, retiring early etc. You should give priority to building an emergency fund which acts as a nest egg to help you manage any unforeseen circumstances that require financial intervention eg losing your phone etc.

The 50/30/20 budgeting rule helps you have enough to pay your bills, have some fun, and save for your dreams. By allocating 50% of your income to needs, 30% to wants, and 20% to savings, you create a balanced financial plan that ensures you’re living well today while securing your future.

An emergency fund lays the foundation for long-term investing and helps you avoid getting into debt in case an emergency arises. It gives you peace of mind to be able to confidently save and invest for a better tomorrow.

Your emergency fund is like your peace of mind account. Having this fund in place means that if a crisis arises, you can navigate through it calmly and confidently. You won’t be forced into debt or make rushed financial decisions that hurt you in the long run. Aim to save enough to cover 3 – 6 months of living expenses in a high yield savings a/c or MMF.

To keep on track you should ensure that you do not use more than 25% of your net income on paying debt. This is known as the debt to income ratio. Tracking helps us avoid using too much of our income to pay debt and protects us from falling into a debt trap.

Of importance is also the house affordability ratio which refers to the portion of a household’s monthly income being used to pay for rent or mortgage. You should also keep this below 25%.

“When your money is in balance, you will always have enough to pay your bills, have some fun and save for your dreams.”

CEO & Co-Founder, Abojani Investment

Robert Ochieng is a visionary entrepreneur and the co-founder of Abojani Investment, a leading financial education platform in Kenya that has empowered over 20,000 Africans to embark on their investment journeys. As CEO, he has demonstrated an unwavering commitment to financial literacy, successfully demystifying money and investments and making them accessible and relevant to individuals from all walks of life.

Running Thriving Investment Communities

Robert’s influence extends well beyond Abojani Investment’s core offerings. He has actively fostered a sense of community by running investment forums and groups with a vast following of over 300,000 Africans. These communities provide a safe space for individuals to exchange ideas, share experiences, and support each other on their investment journeys.

Vision for the Future

As co-founder of Abojani Investment, Robert envisions a financially empowered Africa. He strives to expand the reach of his financial education initiatives, enabling millions more to gain the knowledge and confidence needed to achieve their financial goals. His vision is to create a society where every individual has the tools and understanding to build lasting wealth and prosperity.

Professional Background

Robert Ochieng is a highly accomplished CEO at the helm of Abojani Investment, an investment and advisory firm in Kenya. He is a seasoned professional with over 14 years of experience in IT, Finance, and leadership.

His career includes key roles at prominent institutions such as Equity Bank, Gulf African Bank, Guaranty Trust Bank (GTBank) and Airtel.

Robert’s expertise has also been sought after by the National Treasury for consultancy on planning and budgeting systems, showcasing his exceptional knowledge and skills in the field. Passionate about driving meaningful conversations and collaborations between academia, industry, and the public sector, Robert actively engages in research projects focusing on digital transformation within the financial services sector. With his visionary leadership and strategic insights, Robert Ochieng continues to make a significant impact in the business world.